MacMillan Supply Chain: Revolutionizing 3PL Services for Ecommerce Success

A quick summary and overview MacMillan Supply Chain Group offers…

A quick summary and overview MacMillan Supply Chain Group offers…

A quick summary and overview MacMillan Supply Chain Group is…

A Quick Summary and Overview Reverse logistics is a critical…

A Quick Summary and Overview As Black Friday evolves into…

The U.S.-Iran conflict has become a major supply chain risk story because it affects the Strait of Hormuz, one of the world’s most important energy and shipping corridors. Reuters reports that vessel traffic through Hormuz has fallen sharply from normal levels, while thousands of seafarers have been stranded and shipping companies remain cautious about resuming normal operations. That kind of disruption can ripple into fuel prices, freight rates, insurance costs, transit reliability, and inventory planning across global supply chains. For importers, exporters, retailers, and manufacturers, the real issue is not politics. It is operational resilience.

Global supply chains do not need a direct hit to feel pressure. They only need a major chokepoint to become unstable.

That is why the U.S.-Iran conflict matters to businesses far beyond the Middle East. The Strait of Hormuz is one of the world’s most important maritime routes for oil and LNG, and Reuters reports that recent disruption there sharply reduced vessel traffic and stranded hundreds of ships and around 20,000 crew in the Gulf. Even with talk of a ceasefire, shipping activity has remained well below normal because carriers are still worried about safety, seizures, mines, and fast-boat threats.

For supply chain teams, the smarter question is not who is right. It is what happens to cost, lead time, and continuity if disruption lasts longer than expected. That is the lens this article uses.

The Strait of Hormuz matters because a large share of global oil and LNG moves through it. Reuters reports that the conflict has disrupted roughly a fifth of global oil flows and pushed shipping companies to slow or avoid normal passage through the corridor. When that happens, the impact is not limited to energy traders. It spreads into trucking, ocean freight, air cargo, manufacturing, procurement, and retail replenishment.

When traffic through a route this critical becomes unstable, supply chains usually feel it in several places at once:

Those are the issues most businesses should be watching now.

One of the fastest ways the conflict affects supply chains is through fuel. Reuters reported that oil prices jumped on renewed uncertainty around Hormuz and that the conflict has already been feeding broader price pressure in business surveys. Higher diesel, marine fuel, and jet fuel prices can raise trucking, ocean, and airfreight costs even for companies with no direct sourcing in the region.

Shipping companies do not need a full closure to change behavior. Reuters reported that only a handful of ships passed through Hormuz in a 24-hour period compared with a normal daily average around 140, while alternate nearby routes could not handle normal traffic volumes. That means even a technically open corridor can still operate like a constrained one.

When carriers delay sailings, wait offshore, or reroute cargo, lead times start stretching. Reuters has described stranded vessels, near-standstill traffic, and ongoing safety concerns despite temporary truce language. For supply chain teams, that means historic transit assumptions may no longer be reliable.

Conflict-related maritime risk almost always drives up insurance. Reuters reported that war-risk premiums for Gulf shipping surged by more than 1000% in some cases as insurers repriced exposure. Those costs can show up directly in freight quotes or indirectly through carrier surcharges and tighter capacity.

Reuters also reported that the conflict has been pushing up input costs, slowing factory activity, and adding pressure across the global economy. That means the issue is not just transport. It can also affect packaging, manufacturing inputs, procurement budgets, and consumer demand patterns at the same time.

Industries with high transport or production energy use usually feel the impact first. That includes manufacturing, food production, chemicals, distribution, and bulk goods. When diesel, marine fuel, and power-linked costs rise, margins can tighten quickly.

Retailers and consumer goods companies can be affected through inbound freight costs, packaging costs, and replenishment timing. Even if the finished product does not come from the Middle East, upstream materials and freight networks can still be exposed to fuel and capacity shocks.

Complex manufacturing sectors are especially vulnerable when lead times become unstable. If inbound materials are delayed or freight costs spike, production planning becomes harder and just-in-time models come under pressure. Reuters’ coverage of rising input costs and disrupted logistics supports that broader industrial risk.

Perishable supply chains are exposed because time matters more. If carriers slow down, reroute, or reduce service reliability, spoilage risk and cold-chain cost can rise. That is especially important when maritime schedules become harder to predict.

Fuel, freight, and surcharge assumptions can change faster than normal. Reuters reported oil spikes and broader price pressure tied to the conflict.

Historic transit averages can become unreliable when carriers slow or avoid risky corridors. Reuters reported traffic through Hormuz dropping far below normal levels.

If transit times stretch, reorder points and safety-stock assumptions may no longer protect service levels. Reuters linked the conflict to delivery delays and global logistics disruption.

Longer and less predictable delivery windows can weaken fill rates, OTIF performance, and customer confidence. That becomes more likely when routes remain open only in name but not in stable practice.

When businesses try to protect service levels during disruption, they often shift to more expensive transport options, which can quickly erode margins.

If one route, one region, or one sourcing assumption can disrupt the whole network, the issue is not only the conflict. It is overdependence.

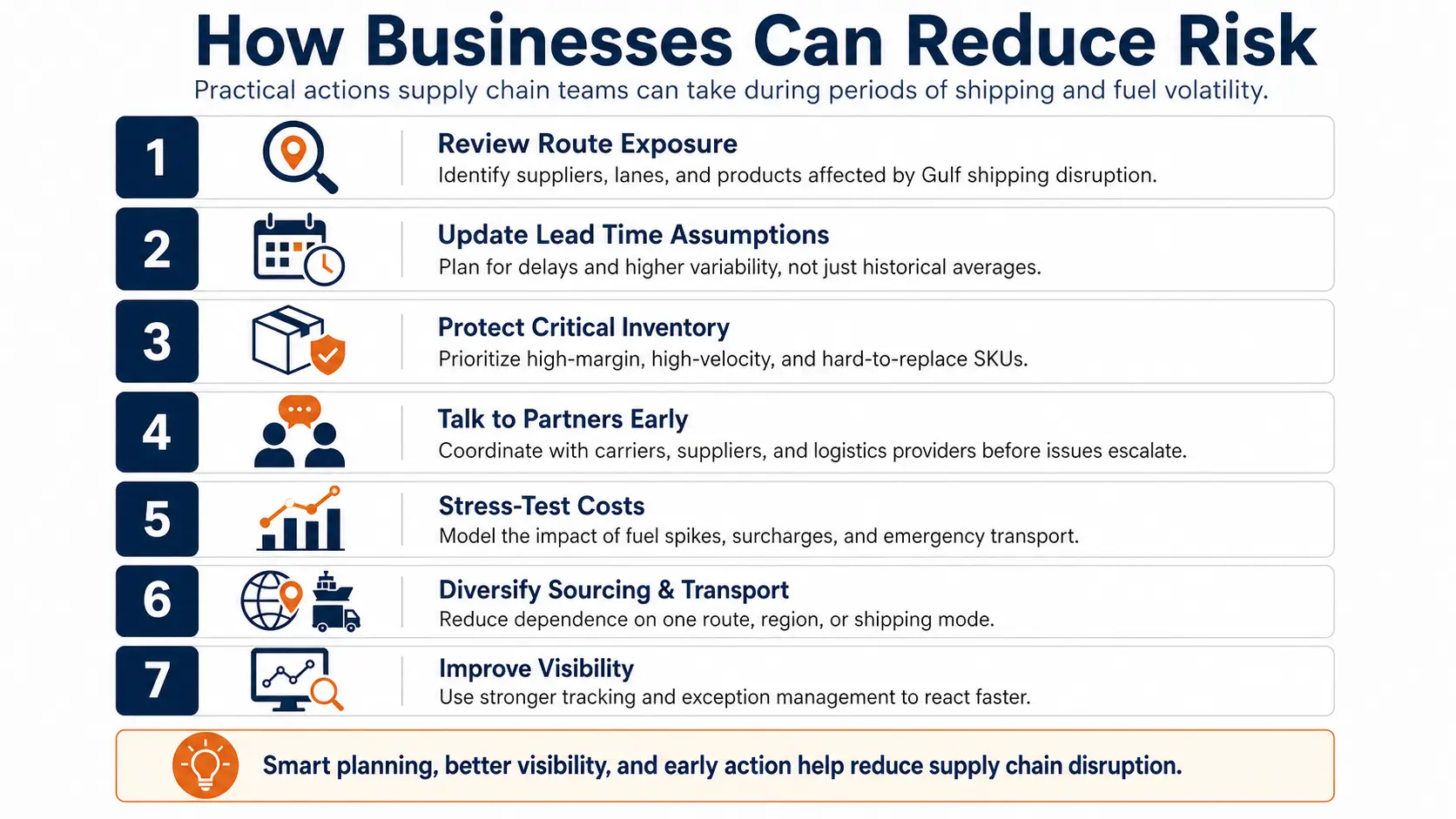

Map which suppliers, products, or lanes depend directly or indirectly on Gulf shipping, energy-sensitive transport, or longer international routings.

Do not rely only on historic averages. Build scenarios for partial disruption, longer delay, and greater variability. Reuters’ coverage suggests that “open” does not always mean “normal.”

Focus on high-margin, high-velocity, hard-to-replace, or customer-critical products first.

Get updates on surcharges, equipment availability, routing risk, and service changes before they become urgent.

Review how fuel spikes or emergency transport would affect landed cost and cash flow.

If one disruption can destabilize the entire network, the operating model may be too concentrated.

Longer and more volatile routes require stronger shipment tracking, milestone updates, and faster response to delays.

The U.S.-Iran conflict increases global supply chain risk because it affects one of the world’s most important shipping and energy corridors. The biggest issue for most businesses is not direct exposure to the conflict itself. It is indirect exposure through fuel volatility, ocean disruption, longer lead times, insurance pressure, and weaker planning reliability. Reuters’ reporting shows that those effects are already visible in vessel flows, insurance pricing, and broader business cost pressure.

The businesses that respond best are usually the ones that move early: reviewing route exposure, updating lead-time assumptions, protecting key inventory positions, and strengthening coordination across suppliers and transport partners.